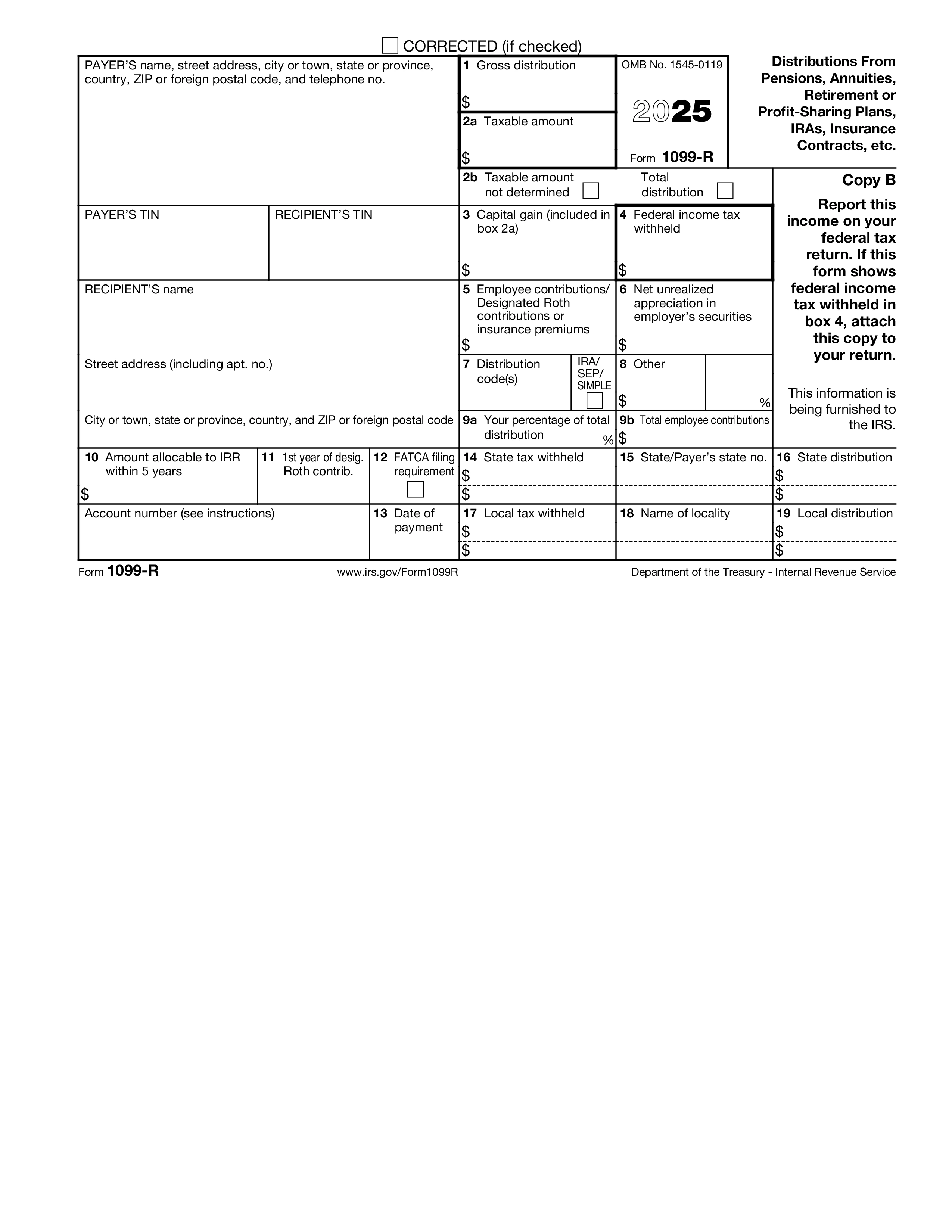

Lomake 1099-R, Osuudet eläkkeistä, eläkkeistä, eläke- tai voitonjakosuunnitelmista, IRA-sopimuksista, vakuutussopimuksista jne., on tietojen palautusmaksun maksajien myöntämä eläke- ja vakuutuksiin liittyvien tilien jakaumat. Se kattaa bruttojaon, verotettavan osuuden, liittovaltion ja osavaltion ennakonpidätyksen, jaon tyypin (varhainen, normaali, kierrätys, muuntaminen, RMD, vammaisuus, kuolema) ja taustalla olevan perusteen (tileillä, jotka sisältävät verojen jälkeistä rahaa). Vastaanottaja käyttää numeroa 1099-R ilmoittaakseen jakelun lomakkeella 1040 ja tarvittaessa lomakkeella 5329 mahdollisten ylimääräisten rangaistusverojen osalta.

Suunnitelmien ylläpitäjät, IRA:n omaisuudenhoitajat, vakuutusyhtiöt, annuiteettien myöntäjät ja muut maksajat antavat lomakkeen 1099-R kaikille, jotka saavat 10 dollaria tai enemmän eläketililtä, eläkkeeltä, annuiteettilta tai vakuutussopimukselta vuoden aikana. Vastaanottajia ovat RMD:t ottavat eläkeläiset, työntekijät, jotka siirtyvät 401(k) IRA:lle, edunsaajat, jotka saavat perinnöllisiä tilijakeluja, veronmaksajia, jotka tekevät Roth-muunnoksia, ja kaikki, jotka tekivät ennenaikaisen noston. Jokainen erillinen jakelutapahtuma yhdeltä maksajalta esiintyy tyypillisesti yhdessä 1099-R:ssä; useat tilit tuottavat useita lomakkeita.

Laatikko 7 sisältää yhden tai kaksi jakelukoodia, jotka kertovat IRS:lle, kuinka jakelua tulee käsitellä. Yleiset koodit: 1 = varhainen jakelu, ei tunnettua poikkeusta; 2 = varhainen jakelu, poikkeus koskee (kuten vammaisuus, SEPP, 55 vuoden ikäero palvelusta tai ensiasunnon ostaja); 3 = vammaisuus; 4 = kuolema; 7 = normaalijakauma (ikä 59½ tai vanhempi); G = suora kierrätys ja kierrätysosuus; H = nimetyn Roth-tilin jakelun suora siirtyminen; B = nimetty Roth-tilin jakelu; Q = hyväksytty Roth IRA -jakelu; T = Roth-jakauma, poikkeus koskee. Koodi määrittää, onko jakelu verollista, 10 %:n sakkoa vai onko se ilmoitettava lomakkeella 5329.

Maksajat toimittavat kopion B vastaanottajille tammikuun 31. päivään mennessä. Kopio A toimitetaan IRS:lle 28. helmikuuta mennessä paperilla tai 31. maaliskuuta sähköisesti. Arkistijoiden, jotka antavat 10 tai enemmän minkä tahansa tyyppistä tietopalautusta, on toimitettava sähköposti. Vastaanottajat käyttävät lomaketta 1099-R täyttääkseen lomakkeen 1040 rivit IRA-jakoa ja eläke-/eläketuloja varten sekä määrittääkseen, tarvitaanko lomake 5329 mahdolliseen ylimääräiseen rangaistusveroon. Valtion kopiot näkyvät valtion tuloveroilmoituksen alemmissa laatikoissa.

1. Täytä lomake

Täytä tietosi ja tiedot, lisää päivämäärä ja mukauta tarpeen mukaan

2. Lisää allekirjoituksesi

Lisää oikeudellisesti sitova allekirjoitus piirtämällä, lataamalla tai kirjoittamalla

3. Lataa tai jaa

Lomakkeesi on valmis, lataa, jaa linkki tai lähetä sähköpostitse välittömästi