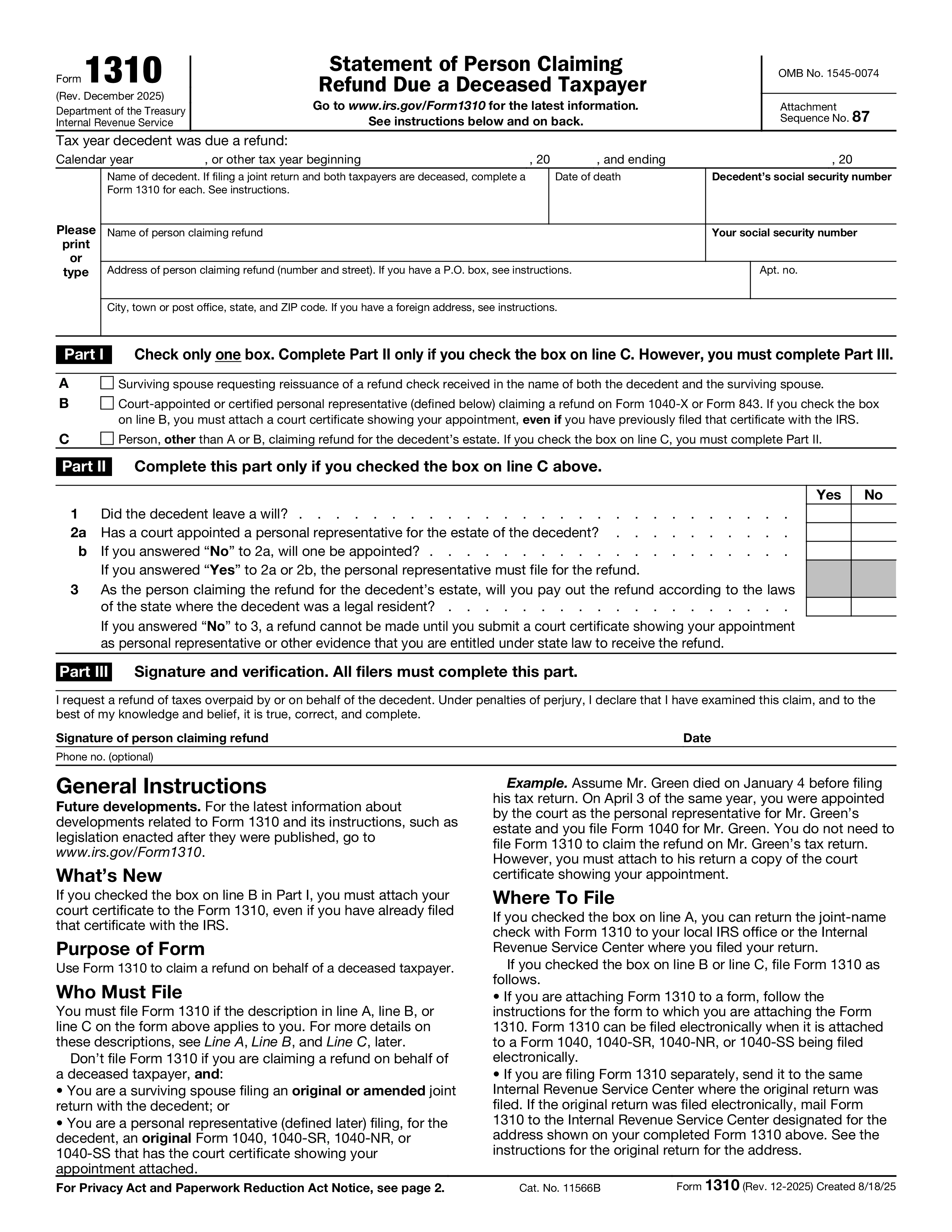

Form 1310, Statement of Person Claiming Refund Due a Deceased Taxpayer, is the IRS form filed when someone is owed a federal income tax refund at the time they pass away. It tells the IRS who is legally entitled to receive the refund and how the check should be issued. Without Form 1310 (or a court-appointed personal representative filing the final return), the IRS won't release the refund — even if the refund is clearly due.

You must file Form 1310 to claim a refund on behalf of a deceased taxpayer unless: you are a surviving spouse filing a joint return with the decedent and the refund check will be issued in both names; or you are a court-appointed personal representative filing the original Form 1040 for the decedent and attaching a copy of your court certificate of appointment. In every other situation — surviving spouse filing separately, surviving child, sibling, or other family member, executor without yet-received court papers, or a court-appointed representative filing an amended return — Form 1310 is required.

Part I asks who you are: surviving spouse claiming a refund check based on a return filed by the decedent (Box A); court-appointed personal representative requesting the refund be issued to the estate (Box B); or other person claiming the refund (Box C). The last category requires either a court certificate, a copy of the will, or a sworn statement that you'll pay any required state inheritance and estate taxes on the refund and distribute it according to state law. You'll need the decedent's full name, Social Security number, date of death, and address.

Attach Form 1310 to the decedent's final Form 1040 or 1040-SR (or Form 1040-X if amending) and file it with the IRS service center for the decedent's state. If the refund is for a return that was already filed before the taxpayer passed away, mail Form 1310 alone to the IRS service center where the original return was filed, along with a copy of the death certificate and any required supporting documents. Most refunds claimed via Form 1310 are issued by paper check, payable to the claimant or the estate as identified in Part I. Processing typically takes 6 to 8 weeks but can take longer for complex estates.

1. Completați formularul

Completează detaliile și informațiile, adaugă data și personalizează după cum este necesar

2. Adăugați semnătura ta

Adaugă semnătură cu valoare legală prin desenare, încărcare sau tastare

3. Descarcă sau partajează

Formularul tău este gata, descarcă, partajează linkul sau trimite prin email instant