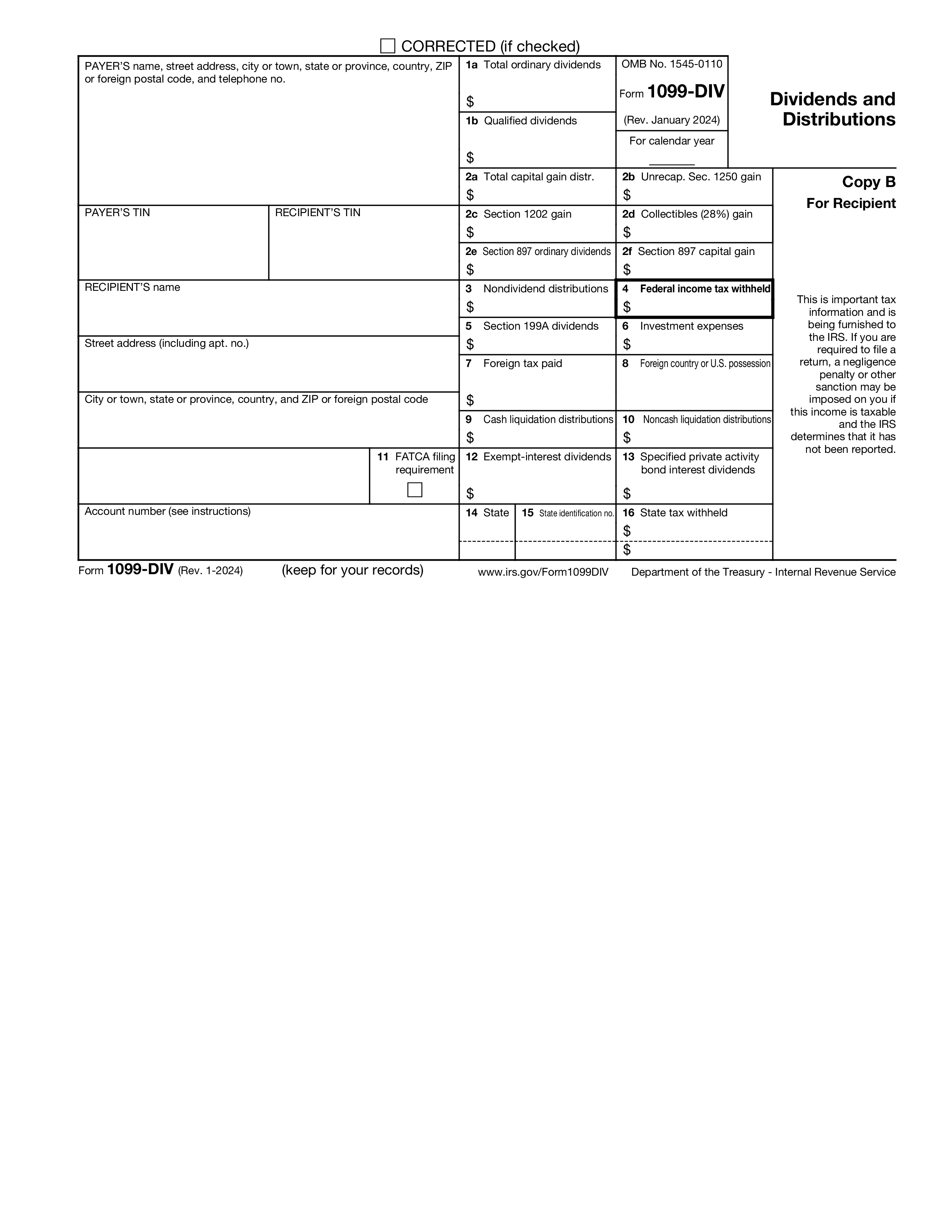

Form 1099-DIV is the information return issued by corporations, mutual funds, REITs, brokers, and other payers to report dividends, capital gain distributions, and certain other distributions paid to investors during the tax year. The form distinguishes ordinary dividends from qualified dividends (which are taxed at the lower long-term capital gains rates), and separates capital gain distributions, nondividend distributions (return of capital), and Section 199A dividends from real estate investment trusts.

Payers — domestic corporations paying dividends, mutual funds and ETFs making distributions, REITs, brokerage firms holding dividend-paying securities in customer accounts — issue Form 1099-DIV. Recipients are individuals, trusts, estates, and other taxpayers who received $10 or more of dividends from a payer during the year. Recipients of $600 or more in liquidation distributions also receive a 1099-DIV. Foreign payments and exempt-interest dividends from municipal bond funds are reported here as well.

Box 1a: total ordinary dividends. Box 1b: qualified dividends (the portion of 1a that meets the holding period and other requirements for long-term capital gains rates). Box 2a: total capital gain distributions. Box 2b–2d: breakouts for unrecaptured Section 1250 gain, Section 1202 gain, and collectibles gain. Box 3: nondividend distributions (return of capital that reduces basis rather than producing taxable income). Box 4: federal income tax withheld. Box 5: Section 199A dividends (qualified REIT dividends). Box 7: foreign tax paid. Box 12: exempt-interest dividends from a municipal bond fund.

Payers must furnish Copy B to the recipient by January 31. Copy A is filed with the IRS by February 28 on paper or March 31 electronically. Filers with 10 or more information returns of any type must e-file. Recipients use the 1099-DIV amounts to complete Form 1040: ordinary dividends on the dividend line, qualified dividends on the qualified dividend line (which routes the tax calculation through the lower capital gains rate worksheet), capital gain distributions on Schedule D (or directly on 1040 in simple cases), and nondividend distributions to adjust the cost basis of the holding.

1. 填写表格

填入您的詳細資料和資訊,新增日期並根據需要自訂

2. 添加您的签名

透過繪製、上傳或輸入新增具有法律約束力的簽名

3. 下載或分享

您的表單已準備就緒,立即下載、分享連結或透過電子郵件發送