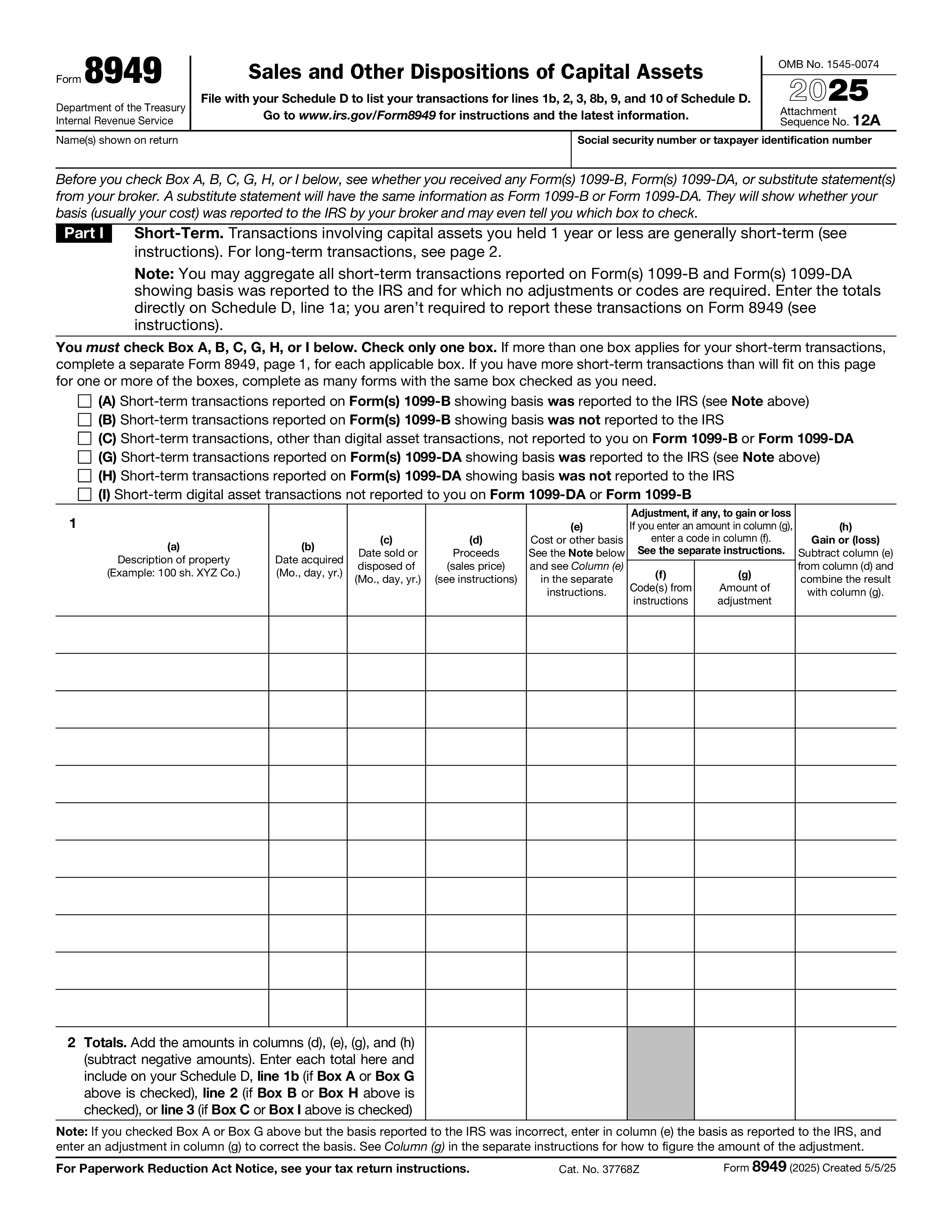

Form 8949, Sales and Other Dispositions of Capital Assets, is the IRS form used to report every sale, exchange, or disposition of a capital asset during the tax year. It lists each transaction individually — date acquired, date sold, proceeds, cost basis, holding period, and any adjustments — so the IRS can match the transactions to Forms 1099-B filed by brokers. Totals from Form 8949 flow into Schedule D, where short-term and long-term capital gains and losses are netted to produce the year's capital gain or loss figure that lands on Form 1040.

Anything classified as a capital asset that you disposed of during the year — sales of stocks, ETFs, mutual funds, and bonds; cryptocurrency and digital asset sales, exchanges, or use to pay for goods; real estate other than your primary residence; collectibles and precious metals; and certain partnership interests. Wash sale adjustments, disallowed losses, accrued market discount, and code adjustments are also entered on Form 8949 using the codes listed in the instructions.

Form 8949 has six categories, split by holding period and reporting type. Short-term (held one year or less): Box A (basis reported to IRS on 1099-B), Box B (basis NOT reported to IRS on 1099-B), Box C (transactions not reported on any 1099-B). Long-term (held more than one year): Box D (basis reported), Box E (basis not reported), Box F (not on 1099-B). Each grouping is totaled separately and carried to Schedule D.

Form 8949 is filed with your annual Form 1040, 1040-SR, or 1040-NR — due April 15 (or June 15 for 1040-NR filers without U.S. wage withholding). When all of your sales fall in Box A or Box D with no adjustments, the IRS lets you skip individual entries and report summary totals directly on Schedule D — but for every other case, each transaction belongs on Form 8949. Most tax software imports transactions directly from broker 1099-B files.

1. 填写表格

填入您的詳細資料和資訊,新增日期並根據需要自訂

2. 添加您的签名

透過繪製、上傳或輸入新增具有法律約束力的簽名

3. 下載或分享

您的表單已準備就緒,立即下載、分享連結或透過電子郵件發送