IRS Form 940 – Fill, Sign and Download | Federal Unemployment Tax

加密並在 15 天後自動刪除

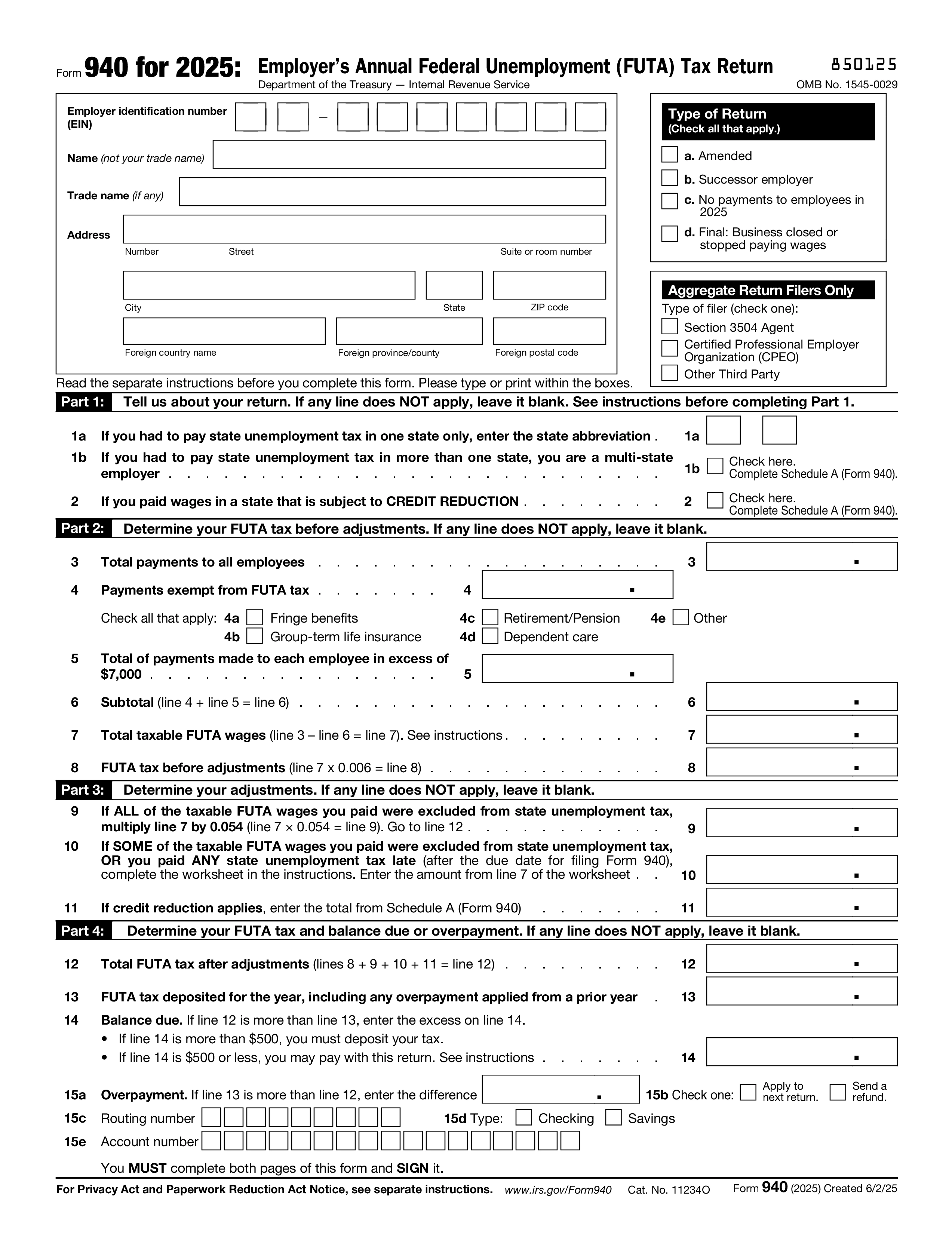

Form 940 is the Employer's Annual Federal Unemployment (FUTA) Tax Return — the federal filing employers use to report and pay FUTA tax. FUTA, together with state unemployment taxes (SUTA), funds the unemployment compensation system that pays benefits to workers who lose their jobs. Unlike Social Security and Medicare tax, FUTA is paid entirely by the employer — not withheld from employee wages.

You must file Form 940 if you paid wages of $1,500 or more in any calendar quarter during the year or the prior year, OR you had one or more employees for at least some part of a day in any 20 different weeks during the year or the prior year. Different thresholds apply to household employers (filed on Schedule H of Form 1040) and agricultural employers (Form 943). Exempt organizations under section 501(c)(3) don't file Form 940 — they're exempt from FUTA.

The FUTA tax rate is 6.0% on the first $7,000 of wages paid to each employee during the year — a wage base that hasn't changed in decades. Employers who pay their state unemployment tax (SUTA) on time and in full receive a credit of up to 5.4%, reducing the effective FUTA rate to 0.6%. States that fail to repay federal unemployment loans (credit reduction states) have a smaller credit, raising the FUTA rate for employers there.

Form 940 is due January 31 for the prior calendar year. If you deposited all FUTA tax on time and in full, the deadline is extended to February 10. FUTA deposits are made quarterly if your accumulated tax exceeds $500; smaller amounts can be carried to the next quarter or paid with the annual return. File electronically through IRS Modernized e-File (MeF) or mail to the address listed in the Form 940 instructions for your state.

1. 填写表格

填入您的詳細資料和資訊,新增日期並根據需要自訂

2. 添加您的签名

透過繪製、上傳或輸入新增具有法律約束力的簽名

3. 下載或分享

您的表單已準備就緒,立即下載、分享連結或透過電子郵件發送