HMRC CWF1 – Fill, Sign and Download | Register as Self-Employed

加密保护,15天后自动删除

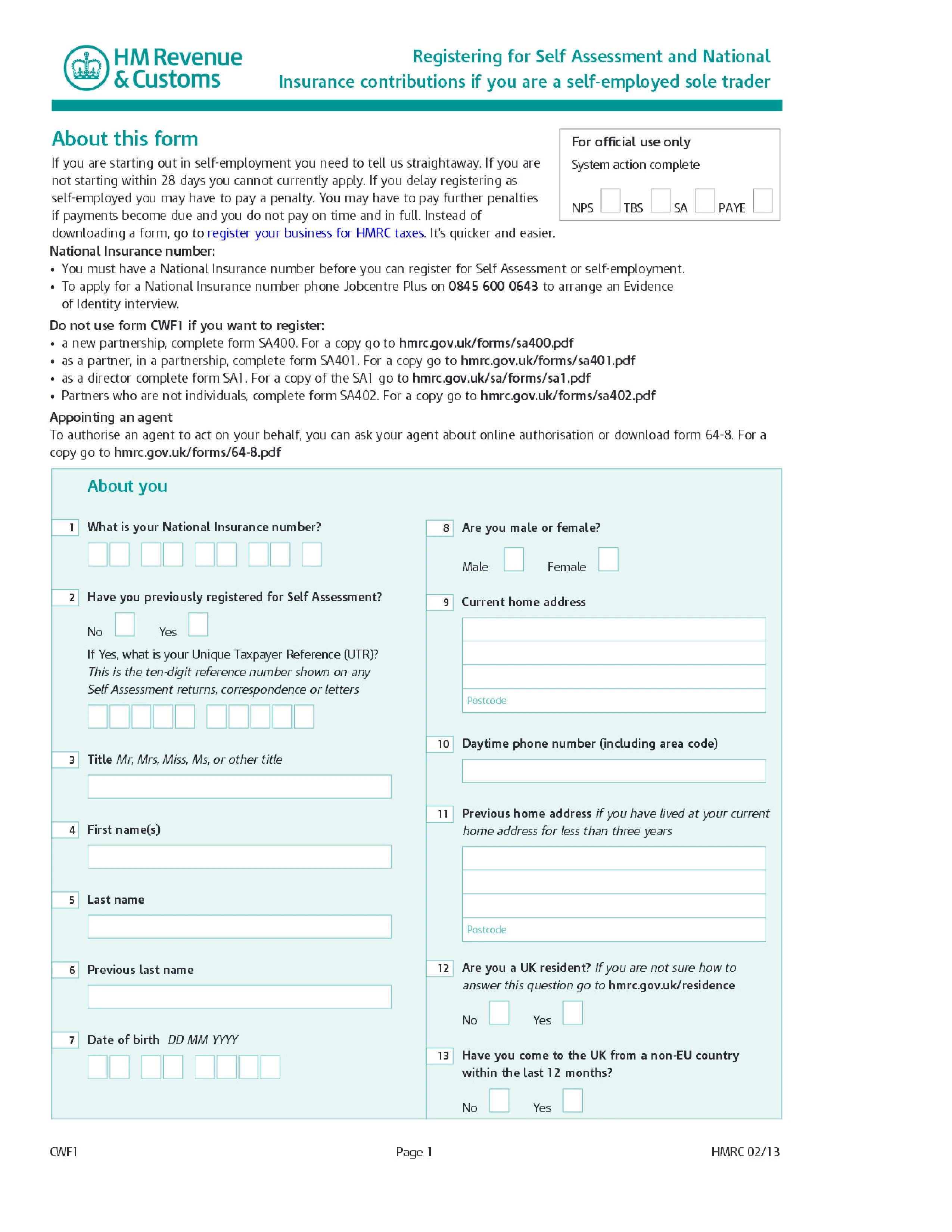

HMRC Form CWF1, Registering for Self Assessment and National Insurance Contributions if You Are a Self-Employed Sole Trader, is the UK registration form used when someone starts working for themselves. It registers the sole trader with HM Revenue & Customs simultaneously for Self Assessment income tax and Class 2 National Insurance contributions — the two obligations that come with self-employed status. After processing, HMRC issues a Unique Taxpayer Reference (UTR) and expects an annual SA100 return with self-employment supplementary pages (SA103).

Anyone starting to work for themselves as a sole trader in the UK must register — freelancers, tradespeople, gig workers, small business owners, consultants, and side-hustlers whose annual self-employment gross income exceeds £1,000 (the trading allowance). Partners in a business partnership use different forms (SA400/SA401). If you're becoming a landlord, high earner, or otherwise need Self Assessment but aren't self-employed, use Form SA1 instead — it doesn't attach Class 2 NI.

Register by 5 October following the end of the tax year in which you started self-employment. For example, if you started in July 2024 (2024/25 tax year), you must register by 5 October 2025. HMRC applies a failure-to-notify penalty to late registrations, calculated as a percentage of the tax due. It's simpler to register within three months of starting to trade to keep everything current.

Personal details (name, address, date of birth, National Insurance number), the date you started (or plan to start) trading, the nature of your business (SIC code, business activity), your business address and trading name if different, your Unique Taxpayer Reference if you already have one, and details of any other UK employment. If you're VAT-registered or plan to register for VAT, that's a separate process (Form VAT1 or online registration through the Government Gateway).

1. 填写表格

填入您的詳細資料和資訊,新增日期並根據需要自訂

2. 添加您的签名

透過繪製、上傳或輸入新增具有法律約束力的簽名

3. 下載或分享

您的表單已準備就緒,立即下載、分享連結或透過電子郵件發送