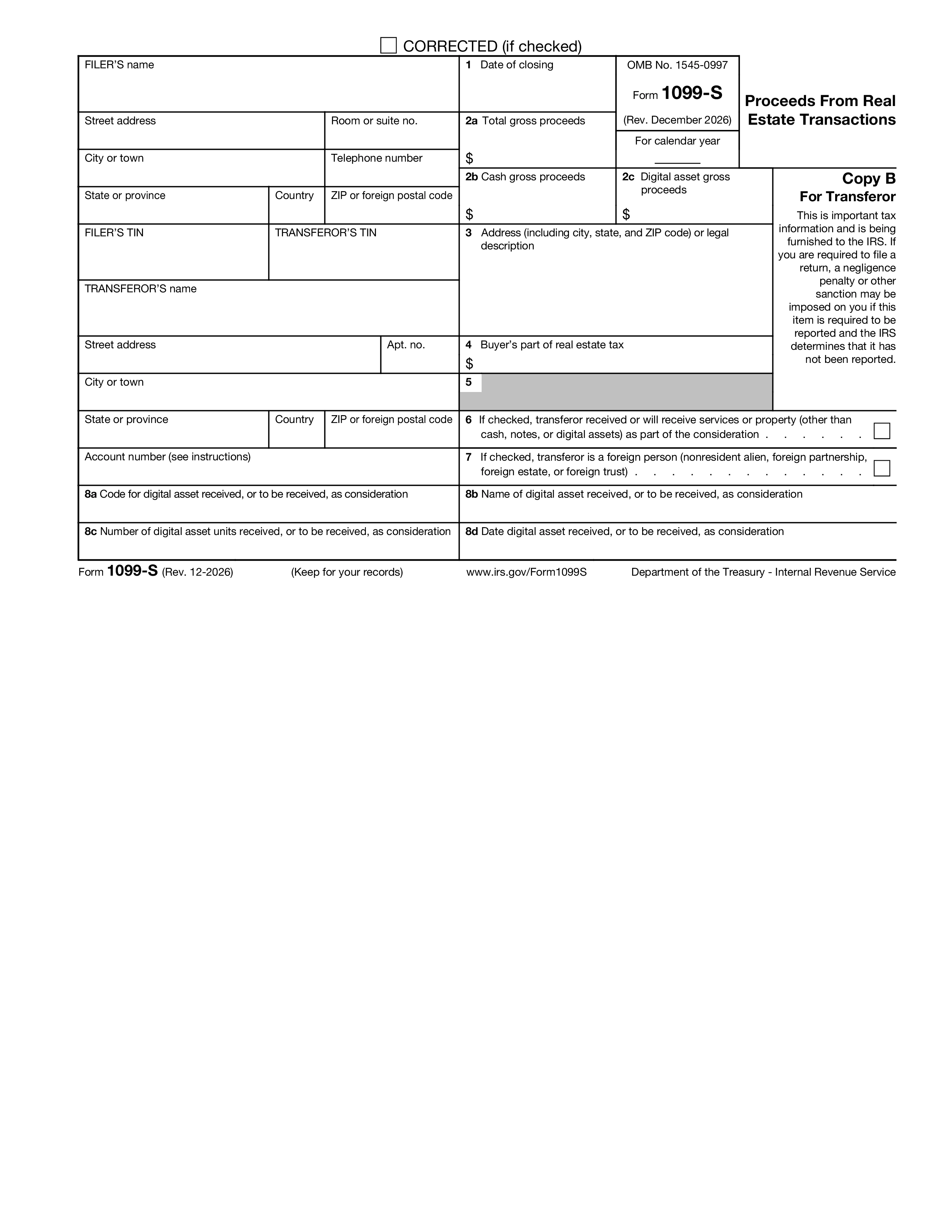

Borang 1099-S, Hasil Daripada Transaksi Hartanah, ialah pulangan maklumat yang melaporkan hasil kasar daripada penjualan atau pertukaran hartanah. "Orang yang melaporkan" — biasanya ejen penutup atau penyelesaian (syarikat hak milik, syarikat eskrow atau peguam yang mengendalikan penutupan) — mengeluarkan Borang 1099-S kepada penjual dan memfailkan Salinan A dengan IRS. Borang melaporkan tarikh tutup, hasil kasar, alamat hartanah atau perihalan undang-undang, dan sama ada sebarang cukai harta diperuntukkan kepada pembeli semasa penutupan. Ia terpakai kepada harta kediaman dan komersial, tanah kosong, kondo, pangsapuri koperasi, perkongsian masa dan kebanyakan kepentingan lain dalam hartanah.

"Orang pelapor" untuk urus niaga hartanah ialah, mengikut keutamaan: orang yang bertanggungjawab menutup urus niaga (biasanya ejen penyelesaian atau syarikat escrow), pemberi pinjaman gadai janji, broker penjual, broker pembeli atau pembeli jika tiada orang lain yang sesuai. Penerima adalah penjual (pemindahan) hartanah. Penjual kadangkala boleh mengelakkan pengeluaran 1099-S untuk jualan kediaman utama yang layak untuk pengecualian penuh Seksyen 121 dengan memberikan pensijilan bertulis tanpa pengiktirafan kepada ejen penutup semasa penutupan — kebanyakan ejen penutup mempunyai borang standard untuk ini.

Penjual melaporkan penjualan pada Borang 8949 (Jualan dan Pelupusan Lain Aset Modal) dan Jadual D Borang 1040 — walaupun tiada cukai terhutang kerana pengecualian jualan rumah Seksyen 121 ($250,000 untuk bujang, $500,000 untuk pemfailan berkahwin secara bersama). Jumlah dalam Kotak 2 Borang 1099-S terdapat dalam lajur Hasil Borang 8949; asas kos penjual (harga belian campur penambahbaikan modal tolak susut nilai) dimasukkan ke dalam lajur Asas Kos. Perbezaannya ialah keuntungan atau kerugian modal, dengan pengecualian kediaman utama digunakan jika ia layak. Hartanah yang dipegang untuk pelaburan atau sewa mengikut aliran yang sama tetapi tanpa pengecualian Seksyen 121.

Orang yang melaporkan mesti memberikan Salinan B kepada pemindah (penjual) selewat-lewatnya pada 15 Februari. Salinan A difailkan dengan IRS selewat-lewatnya pada 28 Februari di atas kertas atau 31 Mac secara elektronik. Pemfail yang mengeluarkan 10 atau lebih maklumat pemulangan apa-apa jenis mesti e-fail. Ambil perhatian bahawa tarikh akhir penerima adalah lewat daripada kebanyakan borang 1099 yang lain (15 Februari lwn. 31 Januari), mencerminkan masa biasa untuk menutup kertas kerja.

1. Isi borang

Isi butiran dan maklumat anda, tambah tarikh dan sesuaikan mengikut keperluan

2. Tambah tandatangan anda

Tambah tandatangan yang mengikat secara sah dengan melukis, memuat naik, atau menaip

3. Muat turun atau kongsi

Borang anda sedia, muat turun, kongsi pautan atau hantar melalui e-mel dengan serta-merta