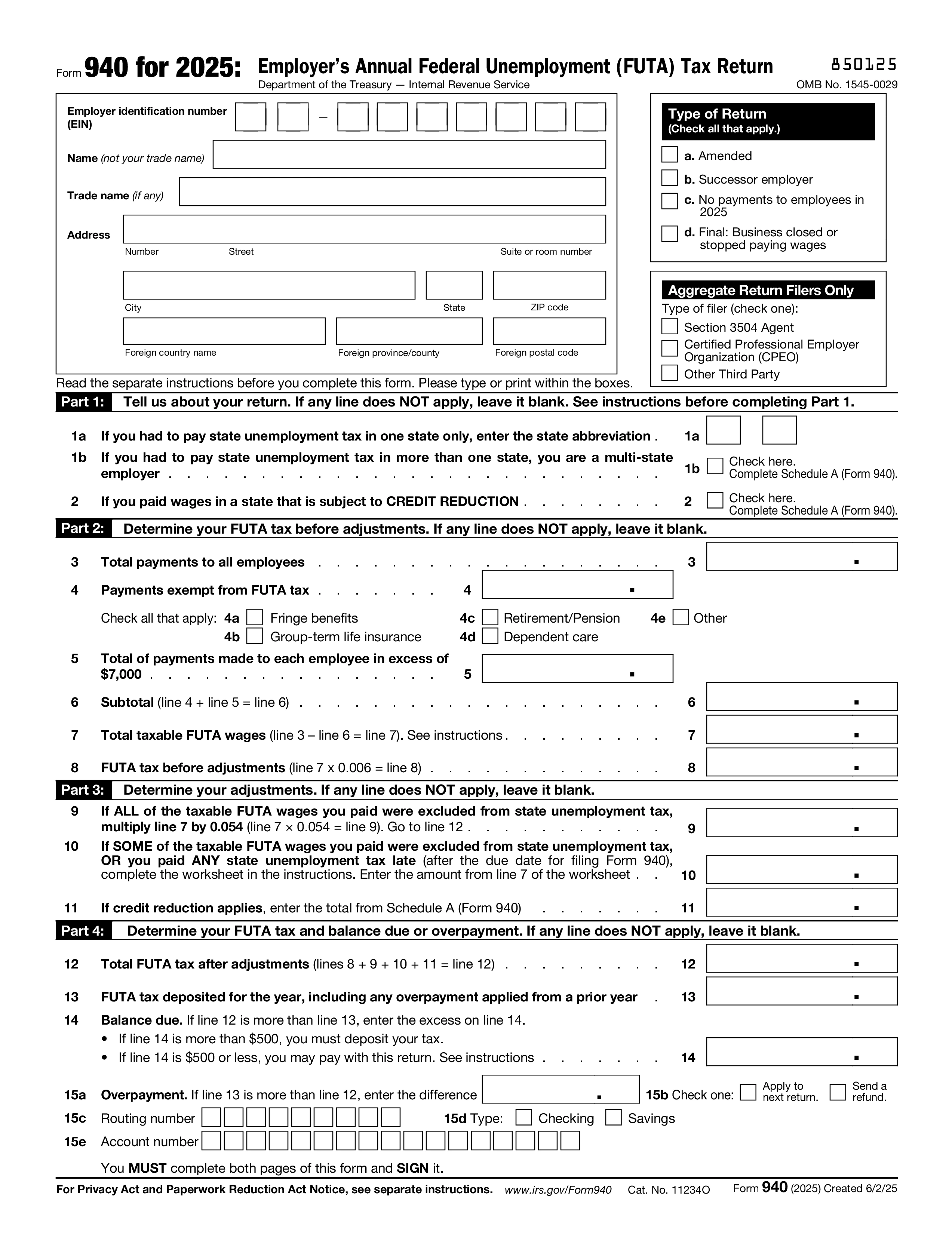

Form 940 is the Employer's Annual Federal Unemployment (FUTA) Tax Return — the federal filing employers use to report and pay FUTA tax. FUTA, together with state unemployment taxes (SUTA), funds the unemployment compensation system that pays benefits to workers who lose their jobs. Unlike Social Security and Medicare tax, FUTA is paid entirely by the employer — not withheld from employee wages.

You must file Form 940 if you paid wages of $1,500 or more in any calendar quarter during the year or the prior year, OR you had one or more employees for at least some part of a day in any 20 different weeks during the year or the prior year. Different thresholds apply to household employers (filed on Schedule H of Form 1040) and agricultural employers (Form 943). Exempt organizations under section 501(c)(3) don't file Form 940 — they're exempt from FUTA.

The FUTA tax rate is 6.0% on the first $7,000 of wages paid to each employee during the year — a wage base that hasn't changed in decades. Employers who pay their state unemployment tax (SUTA) on time and in full receive a credit of up to 5.4%, reducing the effective FUTA rate to 0.6%. States that fail to repay federal unemployment loans (credit reduction states) have a smaller credit, raising the FUTA rate for employers there.

Form 940 is due January 31 for the prior calendar year. If you deposited all FUTA tax on time and in full, the deadline is extended to February 10. FUTA deposits are made quarterly if your accumulated tax exceeds $500; smaller amounts can be carried to the next quarter or paid with the annual return. File electronically through IRS Modernized e-File (MeF) or mail to the address listed in the Form 940 instructions for your state.

1. Điền vào mẫu đơn

Điền thông tin chi tiết và thông tin của bạn, thêm ngày tháng và tùy chỉnh theo nhu cầu

2. Thêm chữ ký của bạn

Thêm chữ ký có giá trị pháp lý bằng cách vẽ, tải lên hoặc gõ

3. Tải xuống hoặc chia sẻ

Biểu mẫu của bạn đã sẵn sàng, tải xuống, chia sẻ liên kết hoặc gửi qua email ngay lập tức