IRS Form 1041 – Fill, Sign and Download | Estates and Trusts

암호화되며 15일 후 자동 삭제됩니다

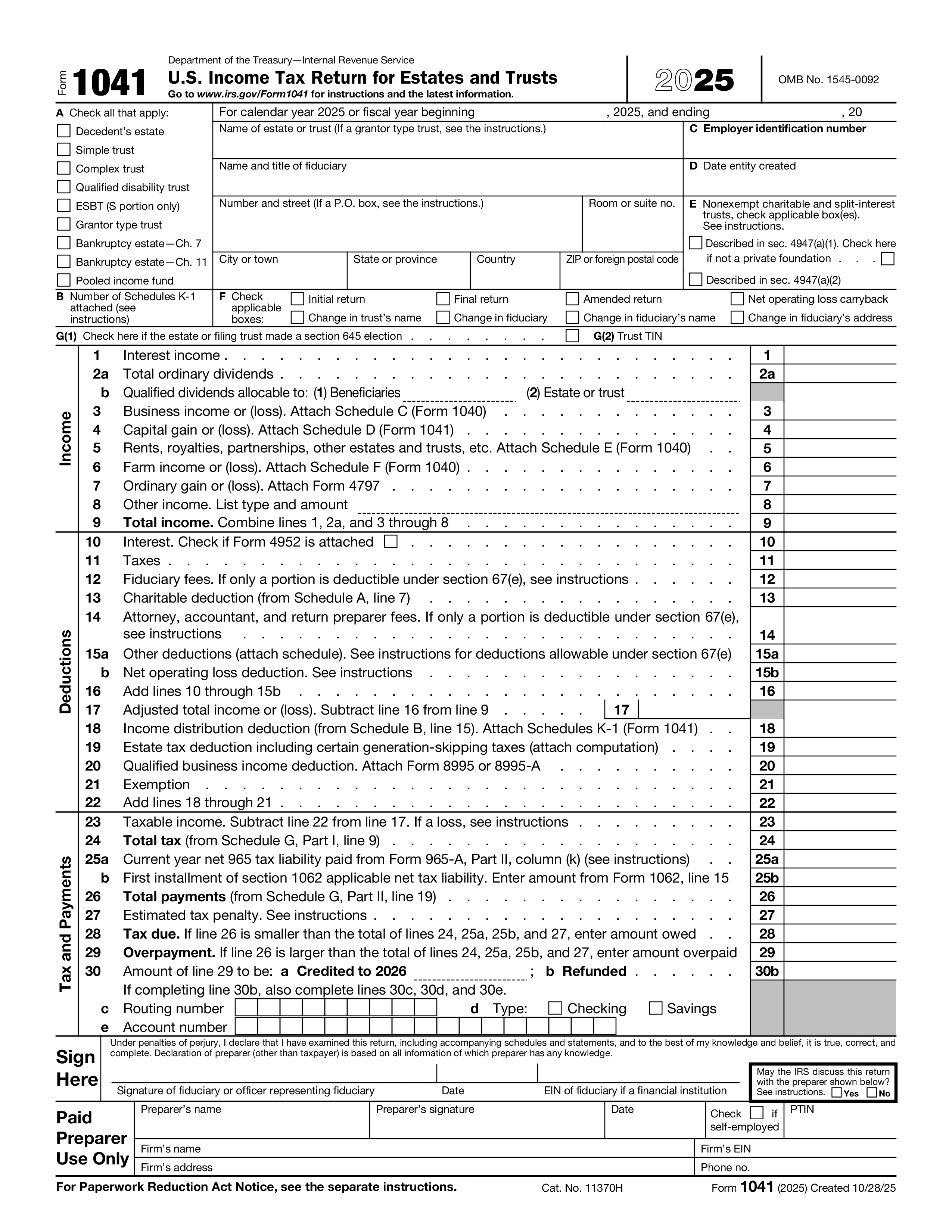

Form 1041 is the U.S. Income Tax Return for Estates and Trusts — the federal return filed annually by the fiduciary of a domestic estate or trust to report income earned, deductions, credits, gains and losses, and any distributions made to beneficiaries during the tax year. It's used by executors of estates and trustees of simple trusts, complex trusts, qualified disability trusts, electing small business trusts, grantor-type trusts (in some cases), and pooled income funds.

The fiduciary of any domestic estate must file Form 1041 if the estate has gross income of $600 or more for the year, or if any beneficiary is a nonresident alien. The fiduciary of a domestic trust must file if the trust has any taxable income, gross income of $600 or more, or a nonresident alien beneficiary. Some grantor trusts file under different rules and may not need Form 1041 if all income is reported on the grantor's personal return.

Have the estate or trust's EIN, governing document (will or trust instrument), prior-year return if applicable, statements of all income received (interest, dividends, capital gains, rental income, business income), records of deductible expenses (fiduciary fees, attorney fees, accounting fees), and details of any distributions made to beneficiaries. You'll prepare Schedule K-1 (Form 1041) for each beneficiary who received a distribution.

Form 1041 is due on the 15th day of the fourth month after the entity's tax year ends — April 15 for calendar-year filers. Estates may choose a fiscal year, so the deadline shifts accordingly. Most trusts must use a calendar year. File electronically through IRS Modernized e-File (MeF) or mail to the service center listed in the Form 1041 instructions. A five-and-a-half-month extension is available by filing Form 7004.

1. 양식을 작성하세요

세부 정보와 정보를 입력하고, 날짜를 추가하고 필요에 따라 사용자 정의하세요

2. 서명을 추가하세요

그리기, 업로드 또는 타이핑으로 법적 구속력이 있는 서명을 추가하세요

3. 다운로드 또는 공유

양식이 준비되었습니다. 즉시 다운로드하거나 링크를 공유하거나 이메일로 보내세요