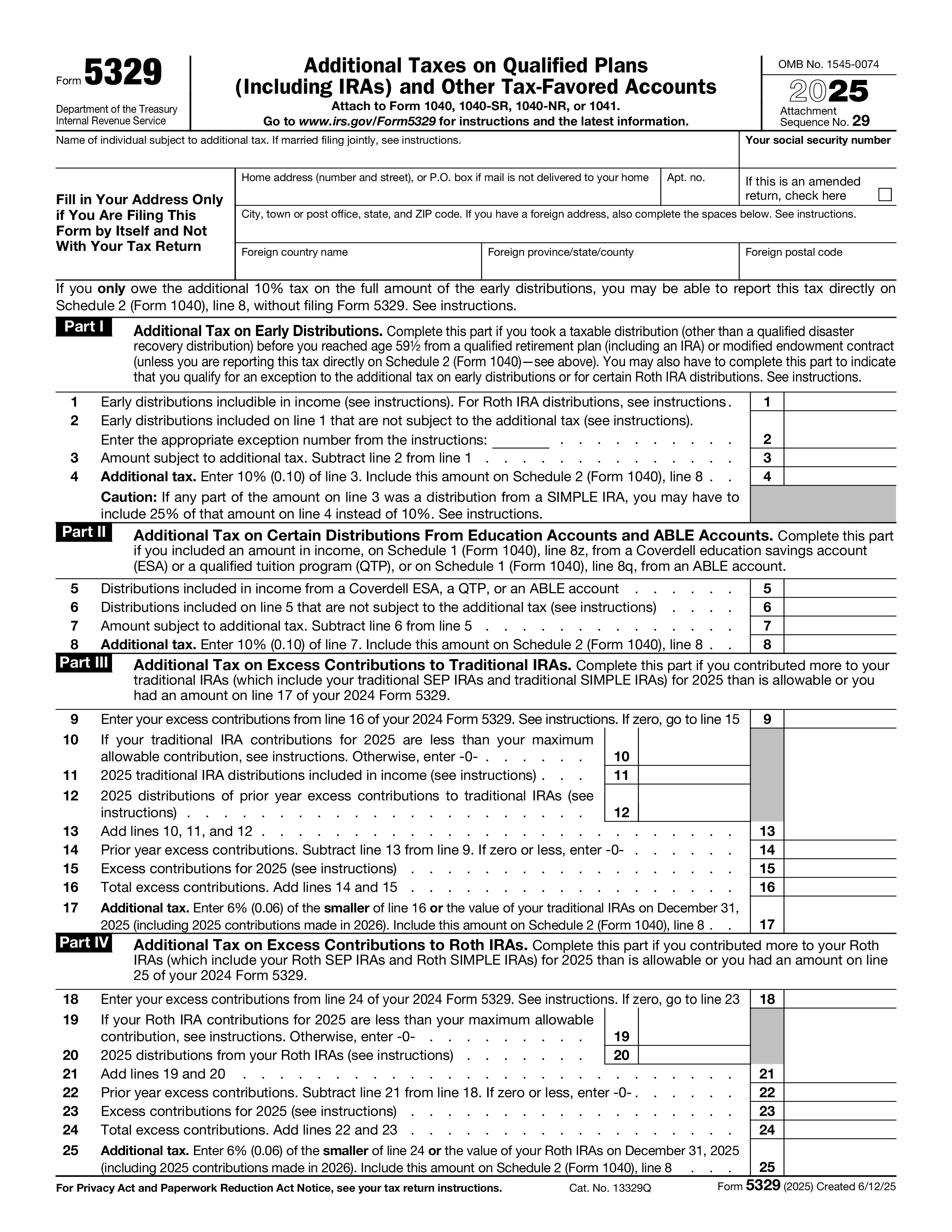

Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts, is the IRS form for reporting penalty taxes and excise taxes related to retirement and tax-advantaged accounts. It covers the 10% additional tax on early distributions from IRAs and qualified retirement plans, the 25% additional tax on early SIMPLE IRA distributions taken in the first two years, the 6% excise tax on excess contributions to IRAs, HSAs, and Coverdell ESAs, and the 25% excise tax on missed required minimum distributions (reduced to 10% if corrected within the IRS correction window). It's also the form you file to claim an exception to those penalties.

File Form 5329 if any of these apply: you took an early distribution (before age 59½) from an IRA, 401(k), 403(b), or other retirement plan and the payer didn't code the distribution as an exception (code 2 on Form 1099-R); you took a distribution that does qualify for an exception (medical expenses, higher education, first-time home purchase, disability, substantially equal periodic payments, etc.) and need to claim it; you contributed more than the annual limit to an IRA, HSA, Roth IRA, or Coverdell ESA; you failed to take a required minimum distribution from a traditional IRA, 401(k), or inherited account on time; or you owe additional tax on Archer MSAs, ABLE accounts, or other tax-favored vehicles.

The 10% additional tax doesn't apply if the distribution qualifies as: medical expenses exceeding 7.5% of AGI; permanent disability; death of the account owner; substantially equal periodic payments (SEPP) over your life expectancy; higher education expenses (IRAs only); first-time home purchase up to $10,000 (IRAs only); unreimbursed health insurance premiums while unemployed; certain birth or adoption expenses up to $5,000; certain federally declared disaster distributions; emergency personal expense distributions up to $1,000 (SECURE 2.0); and several others listed in the instructions. Code each exception with the proper number on Form 5329.

The SECURE 2.0 Act of 2022 reduced the excise tax on missed required minimum distributions from 50% to 25%, and to 10% if the missed amount is taken and a corrected Form 5329 is filed within two years (the IRS correction window). To request a waiver of the penalty for reasonable cause — for example, illness, error by the plan administrator, or other unforeseen circumstances — file Form 5329 with the missed amount, attach a statement explaining the cause and the corrective distribution, and write "RC" next to the line for the excise tax. The IRS routinely waives the penalty when the missed RMD is taken and a reasonable explanation is provided.

1. 양식을 작성하세요

세부 정보와 정보를 입력하고, 날짜를 추가하고 필요에 따라 사용자 정의하세요

2. 서명을 추가하세요

그리기, 업로드 또는 타이핑으로 법적 구속력이 있는 서명을 추가하세요

3. 다운로드 또는 공유

양식이 준비되었습니다. 즉시 다운로드하거나 링크를 공유하거나 이메일로 보내세요