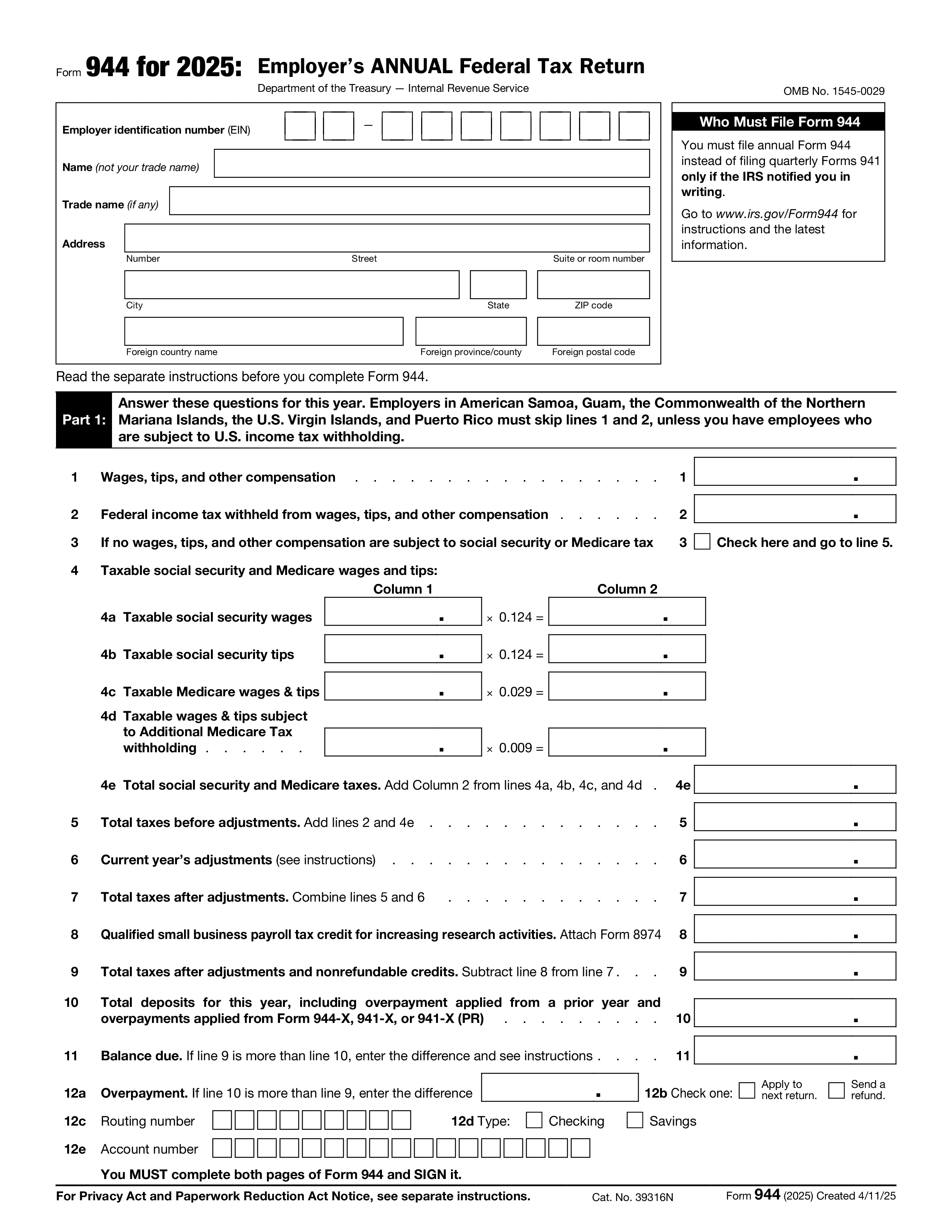

Form 944 is the Employer's Annual Federal Tax Return — designed for the smallest employers who owe $1,000 or less in annual federal employment tax. It consolidates what most employers file quarterly on Form 941 into a single annual filing, reporting Social Security tax, Medicare tax, and federal income tax withholding for the year. The IRS notifies eligible employers in writing if they're approved to file Form 944 instead of Form 941.

You file Form 944 only if the IRS has notified you in writing that you must do so — typically because your annual federal employment tax liability is expected to be $1,000 or less. Employers cannot choose between Form 941 and Form 944; the IRS assigns the filing schedule. If your liability grows above the threshold, you'll get a letter requiring a switch back to quarterly Form 941. New small employers can request to file Form 944 when they apply for an EIN.

Have payroll records for the entire calendar year: total wages, tips, and other compensation paid, federal income tax withheld, Social Security wages and tips, Medicare wages and tips, any sick pay or fringe benefits, and any tax credits or adjustments (such as COBRA premium assistance or qualified small business payroll tax credit). You'll also need your EIN and deposit records for the year.

Form 944 is due January 31 for the prior calendar year. If you deposited all taxes on time and in full, you have until February 10 to file. File electronically through the IRS Modernized e-File (MeF) system or mail Form 944 to the address listed in the instructions for your state. Federal tax deposits are made on a schedule based on lookback liability — monthly or, for very small employers, with the annual return.

1. Wypełnij formularz

Wypełnij swoje dane i informacje, dodaj datę i dostosuj według potrzeb

2. Dodaj swój podpis

Dodaj prawnie wiążący podpis rysując, przesyłając lub wpisując

3. Pobierz lub udostępnij

Twój formularz jest gotowy, pobierz, udostępnij link lub wyślij przez e-mail natychmiast