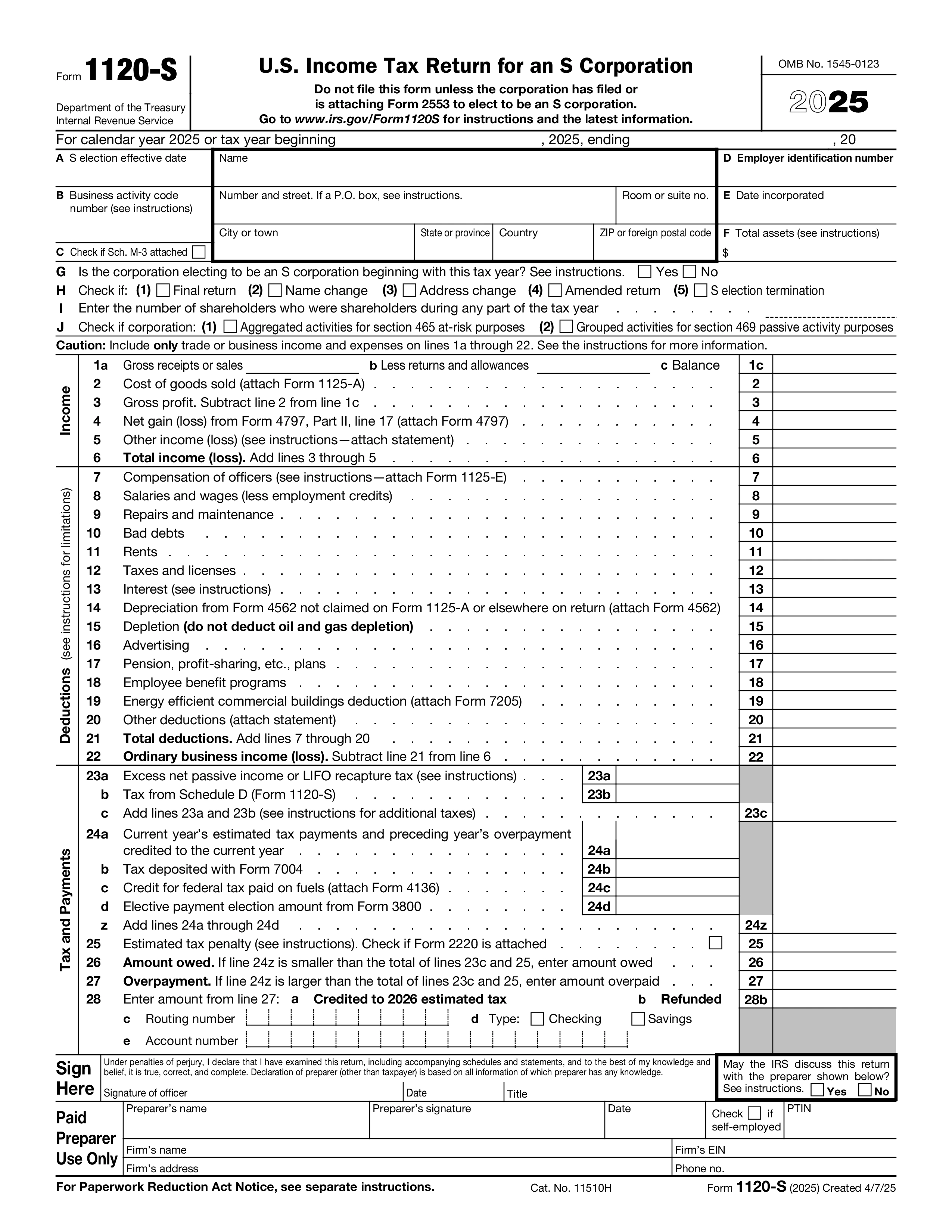

Form 1120-S is the U.S. Income Tax Return for an S Corporation — the federal return filed annually by every S corp to report income, losses, deductions, credits, and distributions to shareholders. Unlike a C corp, an S corp is a pass-through entity for federal income tax purposes: income and deductions flow through to shareholders, who report their share on their personal returns. The S corp itself generally pays no federal income tax.

Every corporation that has filed Form 2553 and is recognized as an S corporation by the IRS must file Form 1120-S annually for as long as the S election is in effect. This includes S corps with no activity for the year, S corps operating at a loss, and S corps in the process of dissolution. Single-member LLCs taxed as S corps file Form 1120-S, not Schedule C.

Have the corporation's financial statements, payroll records (including reasonable compensation for shareholder-employees), depreciation schedules, prior-year return, and a list of all shareholders with their ownership percentages and basis information. You'll prepare a Schedule K-1 for each shareholder showing their distributive share of income, deductions, and credits.

Form 1120-S is due on the 15th day of the third month after the S corp's tax year ends — March 15 for calendar-year filers. File electronically through IRS Modernized e-File (MeF) or mail to the service center listed in the Form 1120-S instructions. Each shareholder must receive their Schedule K-1 by the same date so they can complete their personal returns. A six-month extension is available by filing Form 7004.

1. Vyplňte formulář

Vyplňte své údaje a informace, přidejte datum a přizpůsobte podle potřeby

2. Přidej svůj podpis

Přidejte právně závazný podpis kreslením, nahráním nebo psaním

3. Stáhnout nebo sdílet

Váš formulář je připraven, stáhněte, sdílejte odkaz nebo pošlete e-mailem okamžitě